Blockchain technology has been hailed as a disruptive force across various industries, promising decentralization, transparency, and security.

Blockchain applications have rapidly expanded from finance to healthcare, logistics to entertainment. However, despite its immense potential, blockchain faces significant business model challenges that hinder its widespread adoption and sustainable growth.

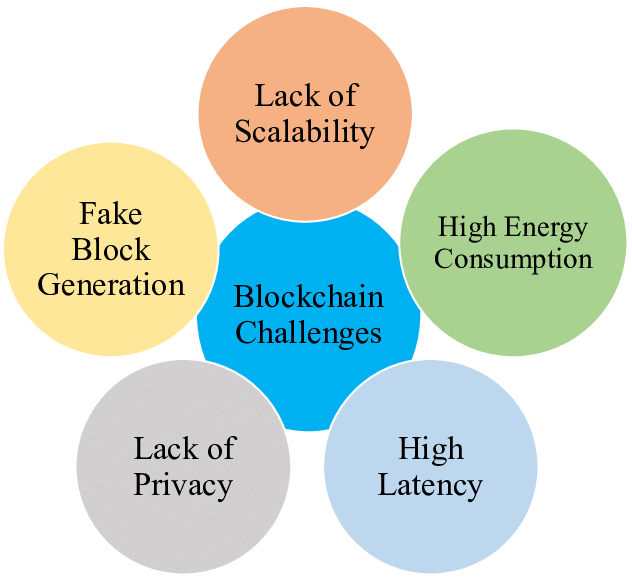

These challenges stem from regulatory uncertainty, scalability issues, energy consumption, integration hurdles, and user adoption barriers.

This article explores these roadblocks in depth and provides insights into potential solutions.

1. Regulatory Uncertainty and Compliance Issues

One of the most pressing challenges blockchain companies face is regulatory uncertainty. Governments and financial institutions are still grappling with how to classify and regulate blockchain-based assets, such as cryptocurrencies, smart contracts, and decentralized applications (DApps).

This ambiguity creates significant risks for businesses operating in the blockchain space.

For example, stringent anti-money laundering (AML) and know-your-customer (KYC) requirements pose obstacles to blockchain-based financial services.

The lack of standardized global regulations results in businesses navigating a fragmented legal landscape, making international expansion difficult.

Additionally, some countries have outright banned or heavily restricted cryptocurrency activities, further complicating the operational environment.

2. Scalability Issues and High Transaction Costs

Blockchain networks, particularly those utilizing proof-of-work (PoW) mechanisms, often struggle with scalability.

Bitcoin and Ethereum, the two most well-known blockchain networks, have faced significant congestion issues, leading to high transaction fees and slow processing times.

These inefficiencies limit blockchain’s practical applications, especially for businesses requiring high-speed transactions, such as e-commerce or real-time payments.

Layer-2 solutions, such as the Lightning Network for Bitcoin and rollups for Ethereum, aim to address these scalability concerns.

However, these solutions are still evolving and require widespread adoption before they can significantly impact business models.

3. High Energy Consumption and Environmental Concerns

Blockchain networks that rely on PoW consensus mechanisms consume vast amounts of electricity. Bitcoin mining alone consumes more energy than some small countries.

This energy-intensive process not only raises sustainability concerns but also affects the financial viability of blockchain businesses.

Companies looking to integrate blockchain solutions must consider these costs and their environmental impact.

Efforts to transition to more energy-efficient consensus mechanisms, such as proof-of-stake (PoS), are gaining traction.

Ethereum’s transition to Ethereum 2.0, which incorporates PoS, is a step in the right direction. However, widespread adoption of greener blockchain solutions remains a challenge.

4. Integration with Existing Systems

For blockchain to achieve mainstream adoption, it must integrate seamlessly with existing business systems and infrastructure.

However, many enterprises struggle to implement blockchain due to compatibility issues with their legacy systems.

The technical complexity and lack of standardized frameworks make integration costly and time-consuming.

Moreover, businesses often hesitate to invest in blockchain technology due to the difficulty in quantifying its return on investment (ROI).

Unlike traditional centralized databases, which have been fine-tuned over decades, blockchain systems are still maturing, making it harder for businesses to justify their implementation.

5. User Adoption and Trust Issues

Despite the enthusiasm surrounding blockchain, many businesses and consumers remain skeptical about its reliability, security, and usability.

Blockchain applications often require a steep learning curve, which limits mass adoption. Moreover, concerns about the security of blockchain wallets, smart contract vulnerabilities, and the irreversibility of transactions make potential users cautious.

To address these concerns, blockchain companies must invest in user education, better UI/UX design, and customer support services.

Simplifying onboarding processes and ensuring that users have access to reliable recovery solutions can improve trust and adoption rates.

6. Lack of Standardized Business Models

Traditional business models, such as subscription-based services or advertising revenue, may not always align with decentralized blockchain ecosystems.

Many blockchain projects rely on tokenomics, where native tokens serve as the primary means of value exchange. However, this model is highly speculative and often leads to market volatility, making long-term sustainability a challenge.

Additionally, decentralized autonomous organizations (DAOs) introduce new governance structures that challenge conventional corporate hierarchies.

While DAOs offer transparency and community-driven decision-making, they also introduce inefficiencies and potential governance disputes, which can affect the stability of blockchain-based businesses.

7. Security Risks and Smart Contract Vulnerabilities

While blockchain technology is inherently secure due to its decentralized nature, vulnerabilities still exist, particularly in smart contracts.

Bugs or poorly written code in smart contracts can lead to devastating security breaches, such as the infamous DAO hack in 2016 that resulted in millions of dollars in losses.

As blockchain adoption grows, so does the sophistication of cyber threats. Ensuring robust security measures, rigorous auditing processes, and ongoing vulnerability assessments is crucial for businesses leveraging blockchain technology.

8. The Challenge of Network Effects

For blockchain-based platforms to succeed, they often require strong network effects, meaning that their value increases as more users participate.

However, achieving these network effects can be difficult, particularly in highly competitive industries.

For example, decentralized finance (DeFi) platforms must compete with well-established traditional financial institutions.

Without widespread adoption, blockchain networks risk becoming isolated or failing to achieve the critical mass necessary for success.

9. Data Privacy and Confidentiality

While blockchain is designed to be transparent, many industries require a level of confidentiality that public blockchains may not provide.

For businesses dealing with sensitive information, such as healthcare records or financial data, ensuring privacy while maintaining transparency is a difficult balance to strike.

Privacy-focused blockchain solutions, such as zero-knowledge proofs (ZKPs) and confidential transactions, are being developed to address these concerns.

However, their implementation is still in the early stages, and businesses must carefully evaluate how to incorporate these technologies while complying with privacy regulations.

10. Talent Shortage and Skill Gaps

Blockchain technology requires specialized knowledge in cryptography, smart contracts, and distributed systems, among other areas.

The shortage of skilled professionals poses a significant challenge for businesses looking to develop and maintain blockchain-based solutions.

To bridge this gap, universities and online education platforms are introducing blockchain-focused courses and certifications.

However, until the talent pool expands, companies may face difficulties in hiring experienced blockchain developers and security experts.

Potential Solutions and the Road Ahead

Despite these challenges, blockchain technology continues to evolve, and businesses are finding innovative ways to overcome these hurdles. Some potential solutions include:

- Regulatory Clarity: Governments and industry stakeholders must work together to establish clear regulatory frameworks that balance innovation with consumer protection.

- Scalability Innovations: The adoption of layer-2 scaling solutions, sharding, and PoS consensus mechanisms can enhance transaction speeds and reduce costs.

- Energy Efficiency: Transitioning to sustainable blockchain networks and utilizing renewable energy sources for mining can mitigate environmental concerns.

- Interoperability Standards: Developing standardized protocols that enable seamless integration with existing systems will encourage broader enterprise adoption.

- Improved User Experience: Simplified onboarding, intuitive interfaces, and better customer support can drive mainstream acceptance.

Conclusion

Blockchain technology holds immense potential to revolutionize industries, but its business model challenges cannot be ignored.

Addressing regulatory uncertainty, scalability issues, energy consumption, integration barriers, user trust, and security risks is crucial for blockchain’s long-term success.

As the technology matures, businesses that adapt to these challenges with innovative solutions will be best positioned to capitalize on blockchain’s transformative power.

The road ahead may be complex, but the rewards for overcoming these hurdles are significant, paving the way for a decentralized and more transparent digital economy.